ISLAMABAD – Each year, millions of overseas Pakistanis send their hard-earned earnings back home, making a vital contribution to the country’s economy. In FY2022-23, Pakistan received over $27 billion in remittances, ranking it among the top six remittance-receiving countries globally.

Today, remittances account for more than 8% of Pakistan’s GDP, serving as a critical lifeline for foreign exchange reserves. Yet, despite their economic importance, Pakistan has not effectively translated these inflows into sustainable national development—unlike several peer nations.

Lessons from Global Success Stories

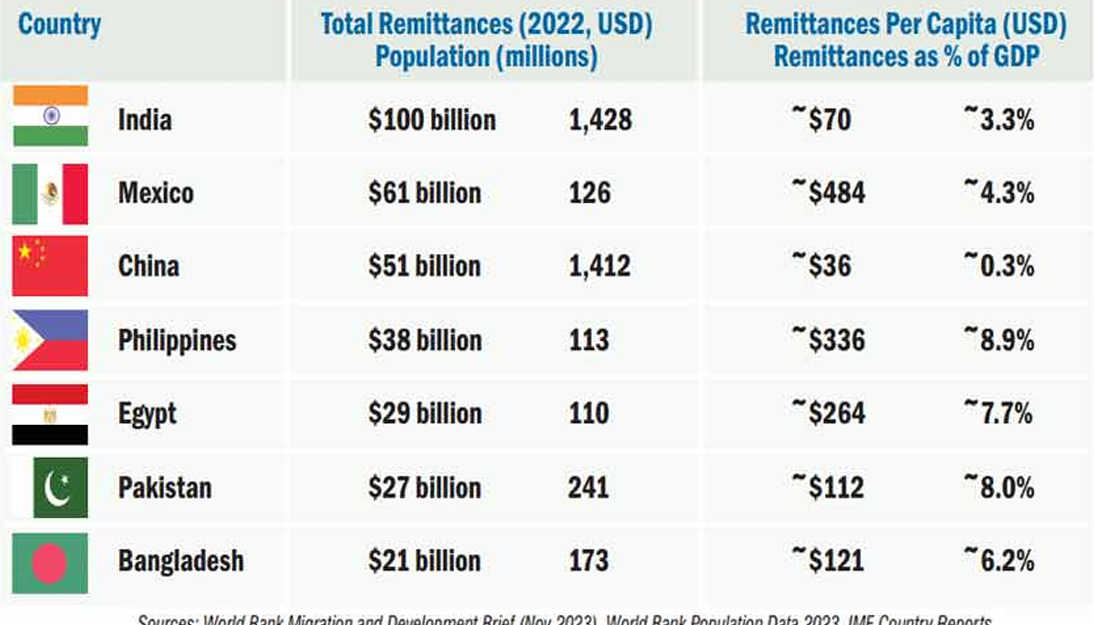

Countries like the Philippines, Bangladesh, India, and Egypt have adopted structured policies to convert remittances into tools for education, entrepreneurship, infrastructure, and industrial growth. Pakistan, by comparison, has largely limited its remittance strategy to short-term foreign exchange needs.

For instance, the Philippines earns about $336 per capita in remittances, compared to Pakistan’s $112, and channels those funds toward productive avenues. Through the Overseas Workers Welfare Administration (OWWA), the country offers skill development, reintegration programs, and investment options in government bonds and businesses for overseas Filipino workers.

Similarly, Bangladesh has simplified money transfers through mobile platforms like bKash, and offers a 2% cash bonus for remittances sent via formal channels. These initiatives have strengthened both economic inclusion and rural development through microenterprise funding.

India has used diaspora investment instruments such as India Development Bonds and Resurgent India Bonds to fund major infrastructure projects. In states like Kerala, tailored programs support the reintegration of returning migrants.

Egypt, on the other hand, encourages investment from its diaspora through real estate incentives and preferential citizenship policies for high-value remitters.

How Pakistan Compares

While remittance inflows remain strong, Pakistan lags behind in policy innovation. According to a 2022 study by the State Bank of Pakistan, over 75% of remittance-receiving households use funds for basic consumption. Only 6% invest in business, and just 2% spend on education or skills development—figures that highlight a missed opportunity for long-term growth.

In times of financial pressure, Pakistan has launched initiatives like Roshan Digital Accounts and Naya Pakistan Certificates, which provide short-term incentives. However, these efforts lack a cohesive institutional framework that ties remittances to national development strategies such as industrial upgrading, digital transformation, or vocational training.

Furthermore, low banking penetration, especially in rural areas, continues to hamper the use of digital remittance channels, limiting financial inclusion and transparency.

A New Framework for Remittance-Led Growth

To unlock the true potential of remittances, Pakistan must shift its approach from reactive to strategic. Here are four key policy recommendations:

1. Establish a Migrant Welfare Authority

A dedicated body should support overseas workers and returning migrants through certification, skills training, reintegration programs, and job matching services. Special focus should be placed on empowering remittance-receiving households through access to education and vocational development.

2. Launch Diaspora-Focused Investment Products

Introduce long-term, flexible investment tools like Pakistan Development Bonds, offering tax incentives and opportunities to invest in infrastructure, education, and public-private ventures. A diaspora equity fund could also allow safe investment in startups and social enterprises.

3. Expand and Incentivize Digital Remittances

Improve mobile banking infrastructure and partner with telecom providers to make remittances easier and cheaper. Like Bangladesh, Pakistan can introduce small cash incentives for using formal channels, which would increase transparency and channel funds toward formal sectors.

4. Ensure Transparency Through Reporting

An annual Remittance Impact Report can help track the effectiveness of policies, understand regional flows, and adjust strategies based on performance. Collaborating with think tanks and universities would provide valuable insights for data-driven policymaking.

The Way Forward

With over nine million overseas Pakistanis, the country has a unique opportunity to harness remittances as a pillar of long-term economic development. The examples of peer countries demonstrate that it’s not just the volume of remittances that matters—but how they are used.

For Pakistan, this means redefining the narrative: from remittances as lifelines to remittances as engines of growth. This will require bold policy reforms, new financial tools, and a clear link between remittance flows and national development goals.

By leveraging this valuable resource strategically, Pakistan can pave the way for a more resilient, inclusive, and forward-looking economy.

Leave a Reply